- Hits: 938

ESG Investment, The future of investment

What is ESG Investing?

ESG (Environmental, Social and Governance) investing refers to a class of investing that is also known as “sustainable investing.” This is an umbrella term for investments that seek positive returns and long-term impact on society, environment and the performance of the business. There are several different categories of sustainable investing. They include impact investing, socially responsible investing (SRI), ESG and values-based investing. Another school of thought puts ESG under the umbrella term of SRI. Under SRI are ethical investing, ESG investing and impact investing.

The Financial Times Lexicon defines ESG as “a generic term used in capital markets and used by investors to evaluate corporate behavior and to determine the future financial performance of companies.” It is used by investors to evaluate corporations and determine the future financial performance of companies. It adds that ESG “are a subset of non-financial performance indicators which include sustainable, ethical and corporate governance issues such as managing a company’s carbon footprint and ensuring there are systems in place to ensure accountability.” They are factors in investment considerations, used in risk assessment strategies incorporated into both investment decisions and risk management processes.

What is the Appeal of ESG Investing?

Many investors are not only interested in the financial outcomes of investments. They are also interested in the impact of their investments and the role their assets can have in promoting global issues such as climate action. One demographic that is particularly attracted to ESG investing is millennials. According to a 2006 study called Cone Millennial Cause Study, millennials are more likely to trust a company or purchase a company’s products when the company has a reputation of being socially or environmentally responsible. Half of those surveyed are more likely to turn down a product or service from a company perceived to be socially or environmentally irresponsible.

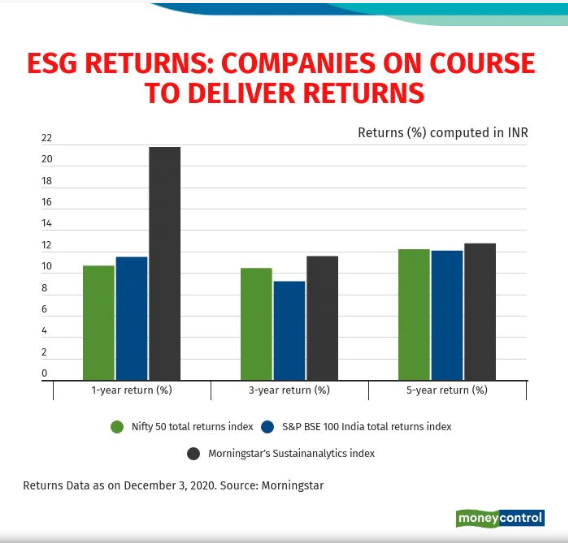

The Rs 30 trillion Indian mutual funds (MF) industry may have seen five ESG-themed MF schemes rolled out so far in 2020. But a wave of ESG investing has been sweeping global markets for some time now.

Data from research firm Morningstar Investment Adviser showed that in October, global assets under management (AUM) with ESG portfolios hit a high of US$1.2 trillion – a quantum increase from $530 million five years ago. Bloomberg reports state that there were 17 ESG exchange traded funds rolled out so far in 2020, compared with 10 in all of 2019. This launches make October the best-ever month for inflows since 2013.

In India however, ESG funds are still in a nascent stage. But investor interest is increasing. There is awareness about ESG in every aspect of conducting business. Society wants to see businesses being more responsible in these areas and it is already visible in lending practices and investor participation globally.

India has a long road ahead in sustainable investing, given the host of mid and small-sized companies that may find it challenging to comply with such norms. But, experts say that the Indian MF industry is moving in the right direction. As more schemes raise money, investor awareness would improve. Companies that have low ESG scores could lose prominence or importance in the investment horizon, even if they generate higher profits. Such companies stand the risk of losing capital flows, especially from FIIs.

So in all ESG is the future of investment. If one is looking at responsible investing than one must apply for the Aditya Birla Sun Life ESG Fund NFO. Call us to apply. NFO closes 18th December 2020.

The ESG theme must be included in the core portfolio. Returns through the ESG themes are expected to be higher than non-ESG funds with same risk profile.